Spend management industry - a SaaS and fintech combination?

Executive summary

Spend management platforms can provide value at a reasonable cost to small, mid and large enterprises. The affordability is the result of cost being spread out to several partners. The platforms monetise several parties involved in the ecosystem as businesses (clients) contribute only 5-20% of overall revenues (refer exhibit 1).

Affordability coupled with various advantages such as transparency, compliance, cost savings on account of vendor aggregation & negotiations, faster approvals etc. are the other benefits which drive the demand of the product. Once a client is onboarded it is difficult for competition to disrupt the service provider as the integration of the platform is very strong with various partners like banks, network providers payrolls, and accounting platforms. Hence, churn rate for spend management platforms is low

Source: Zaggle Investor presentation, Korman Capital

Opportunity size:

Units: Addressable SMEs count is over 3 lakhs in India. Zaggle Prepaid Ocean Services limited (Zaggle), Indian listed spend management platform company, has only 3,000 customers. Hence, penetration of spend management platforms is estimated to be very low. The number of new companies registered every year are growing at ~25% from last 3-years. Further, low-cost base of India shall allow Indian players to tap even global opportunity. United states has ~60 lakh SMEs.

Transaction value: India’s prepaid transaction value stood at USD10billion in FY23/24 and it is likely to grow to USD35billion by FY27. Zaggle boasted of 16% share. Zaggle has recently launched credit card product which is bigger market than the pre-paid cards. On global front, for context, one of the US based company, Bill Holdings, had transaction value of USD266 billion in 2023. Hence, we believe India also has a huge opportunity size for some of the spend management companies like Zaggle.

Growth: Given the low penetration of spend management, increasing number of new companies, and huge potential of transaction volumes (USD35 billion by FY27/28 at an annual growth of over 30%) is likely to result in very high growth of the sector. Globally some startups have grown at over 50% for last 3-4 years. Hence, we believe some select companies in India can also exhibit such high growth rates in mid to long term.

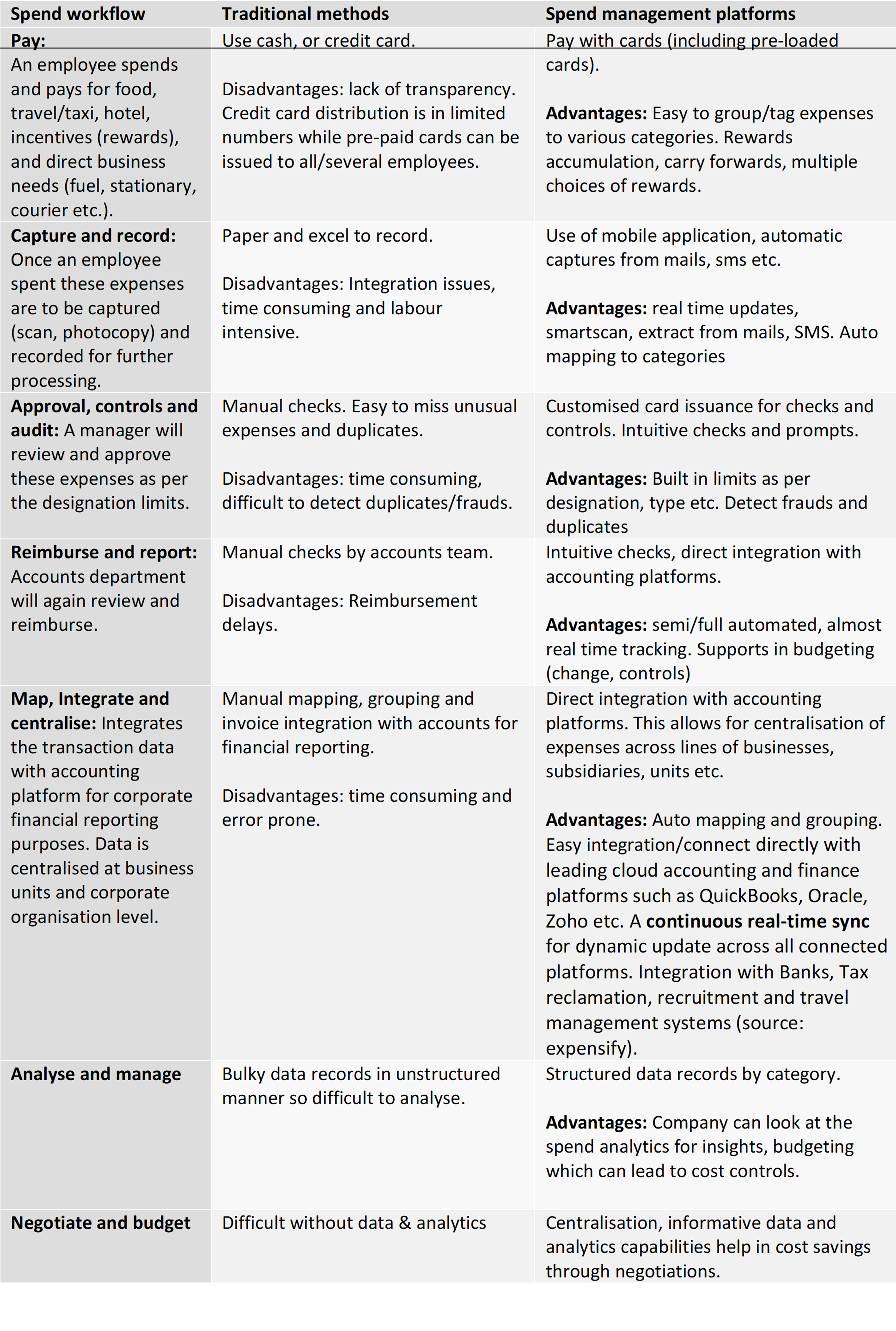

Why spend management is closely integrated to a business

It is important to understand a typical workflow on business spends to understand the integration:

Now we can summarise that a spend management platform provides:

1. Payment instruments

a. Pre-paid cards

b. Credit cards

2. Software platform for

a. Spend analytics, visualisation, budgeting & forecasting

b. Financial reporting - Integration with accounting platforms

c. Vendor integration and centralisation at company and different unit levels

3. Value-added services:

a. Merchant network/integration (Travel, food, fuel – gas stations etc.)

b. Treasury support

c. Small credit period

The spend workflow and services provided by spend management platforms makes it clear how important it is to have a streamlined expense management. This impacts compliance, reporting, cost and budgeting process of a business. In addition, integration of a business with spend management platform is strong owing to integral connect with banks, employees, and accounting platforms. Changing platform also leads to training of employees, cumbersome balance transfers, reconciliation etc. Hence, once a business uses a particular spend platform its stickiness is high. Zaggle’s churn rate is low at 1.5% for last 3-years.

Having established that the value provided by spend management platform is reasonably good, let’s look at some global companies including recently listed Zaggle Prepaid Ocean Services limited.

*Private

Source: Company filings and Korman Capital

Above table consists of 4 listed players and one unlisted player (Pleo). The market cap/valuation of these companies is in USD0.2billion to USD5.3billion range. The average growth rate of these peers is ~30% and median growth is 40%. Pleo, being private, is an outlier in terms of valuation with market cap to sales at 43x vs. rest of the peers are in 1x to 5x range.

Most of these companies, other than Edenred and Zaggle, are loss making. While gross margins are in 40% to 90% range, EBITDA margins are varied with negative to 44%. Edenred is sort of an exception as this being a more established player (over 50 years) and moderate revenue growth. Once a company gains scale margins improve substantially, for example Pleo 3 -years back on USD28 million revenues had 1.6% gross margin, however with USD100 million revenue rate in 2023, it now boasts of 40% gross margins.

Transaction volumes is an important data as a good amount of revenue (up to 80%) is earned from it. Few companies in our peer set have transaction value in USD100 billion to USD300 billion range. Zaggle is currently doing only USD1.2 billion in transaction value. We expect this grow at over 30% CAGR in near future (industry growth in 30% to 40% range).

Triangulating all this to Zaggle:

Franchise: Zaggle, established in 2011, is one of the leading spend management platform with 16% market share in prepaid transaction value and ~20% volume of prepaid card issuance (Source: Frost & Sullivan). The company offers three key products namely: 1) Propel – employee, vendor and channel partner’s reward & recognition platform, 2) Save – an employee reimbursement, and tax benefit solution, and 3) Zoyer: business spends management/accounts payable.

It is worth noting that Zoyer which was launched in 2023, within one year it has contributed ~25% of revenues. Hence, we believe Zaggle has capability to continue to launch innovative products to propel its growth. The other adjacencies which Zaggle can target in future is treasury, fleet management etc.

Growth and profitability: Zaggle reported revenue of INR776 crores in FY24. Management has guided to double its revenues by FY26. We believe this target is in sight as new product (Zoyer – credit card product) which was launched in 2023 has started exceeding prepaid card transaction volumes. In addition, company continues to add new clients. Zaggle is profitable company with EBITDA margin of ~9%. EBITDA margin potential is ~15%, however, given that company is investing aggressively in gaining market share and new product development its margins are suppressed as of now. However, management guides to go back to 15-16% margin levels in 3 to 5-years.

Valuations: The median multiple market capitalisation to sales in our peer set is ~5x. However, private company market valuations are in 10x to 44x as per their last round of capital raise. One of the public company - Coupa was acquired by a private equity at 10x multiple in 2022.

Source: Company filings, various news sources and Korman Capital

We note that the recent global M&A transactions have taken place in 10x to 25x revenue multiples. In India, Happay was acquired by Cred at 18x revenue multiple. Its worth noting that most of these companies were making losses.

Zaggle growing its revenues in 45-50% range with EBITDA margins in 9-10% range, should command a higher revenue multiple of 7x to 10x.

RISKs

1. Highly competitive market. Globally and locally many startups have mushroomed to address this are, some examples are – M2P, Airbase, Zoho, Spendesk. Many of the startups provide initially free services. Hence, this could pressurise margins and revenue growth. Expensify, a US listed company, provides free limited feature access. Only when number of users in organisation increases, user/businesses might end-up paying for it.

2. Technology risk, R&D and new product development costs: Companies need to continue to invest to launch new pruducts and update features. This may lead to suppressed profitability for long periods. Zaggle’s EBITDA margins fell to 9% in FY23 and FY24 from ~16% in FY22 owing to cost related to new product development and amortisation of the same.

3. Regulatory risks: Zaggle earns ~80% of revenues from interchange fee. If there is any regulatory cap on these charges than this might impact Zaggle’s revenue.

Korman Capital Investment Advisors LLP (“Investment Advisor”) is registered with SEBI as Investment Adviser with Registration No. INA000018656. The Investment Adviser got its SEBI registration on December 06, 2023 and is engaged in research and recommendation Services. Investment Adviser aligns its interests with those of the client and seeks to provide the best suited services.

Ø Investment Adviser have no material adverse disciplinary history as on the date of publication of this update.

Ø Investment Adviser has no associates

Ø Investment Advisers or its employee or its associates may have beneficial ownership of 1% or more in the subject company at the end of the month immediately preceding the date of publication of the Investor Update.

Ø Investment Advisers or its employee or its associates does not have any financial interest in the subject company.

Ø Investment Advisers or its employee or its associates have no actual or potential conflicts of interest arising from any connection to or association with any issuer of products/ securities, including any material information or facts that might compromise its objectivity or independence in the carrying on of recommendation services at the time of publication of the Investor Update.

Ø Investment Advisers or its employee or its associates have not received any kind of remuneration or consideration or compensation form the subject company or from anyone in connection with the Investor Update in the past twelve months.

Ø The subject company was not a client of Investment Adviser during twelve months preceding the date of distribution of the Investor Update.

Ø Investment Advisers or its employee or its associates have not served as an officer, director or employee of the subject company.

Ø Investment Advisers or its employee or its associates have not been engaged in market making activity of the subject company