EMS – A baton holder of India’s manufacturing renaissance

Executive summary

India’s EMS industry is growing at a very fast pace owing to localisation drive, and production linked incentives (PLI) by government. The industry growth and margins are driven by company’s position in value chain, end-industry it caters to, vertical integration, and specialisation/customisation of the products. We studied 10 companies in the sector and the standouts are:

Dixon Technologies: Dixon Technologies is a clear winner owing to its strong growth and return metrics. Dixon’s business model is very efficient emanating from its negative working capital model, high level of fungibility of assets, and strong growth.

IKIO Lighting: IKIO stood out due to its high EBITDA margins (~20% vs. industry in 7-15% range) and strong return metrics (ROE/ROCE/ROIC of 20%+). This strength is mainly driven by IKIOs majority of revenue coming from ODM manufacturing, vertical integration and high level of customised solutions. IKIO trades attractive at PE of 32x FY25E vs. peer average of ~70x. However, IKIO ranked 3rd owing to its low growth rate (~25%) vs. peers (~45%).

Source: Korman Capital estimates

Background

Indian Electronic Manufacturing Services (EMS) industry has been growing at over a 30% rate in the recent past and it is expected to continue this pace. The industry is mainly aided by production linked incentives (PLI) by government to reduce India’s import dependence on electronic items. The poster boy of electronics manufacturing renaissance has been Dixon Technologies which has seen its revenues growing ~10x in 6 years (~3,000 crores in FY2019 to ~30,000 crores by FY25E). The success of Dixon and the industry has resulted in several companies getting listed on Indian bourses. From investors perspective, there was hardly any choice few years back but now there over dozens of companies to choose from.

The earnings growth and margin drivers of a company depend on 1) where company fits into the value chain, 2) what end-industry they cater to, and 3) other factors such as level of vertical integration and customisation requirements of the products. Let’s delve into these factors further:

Value chain

The table below summarises the different stages of value chain along with different levels of margins and volumes. In addition, industry has different capabilities in each of the stages.

Source: EY, Korman Capital

Product design and development Only a few EMS players are involved in design and development who are called as original design manufacturers (ODM). Though specialisation and differentiation is low in ODM it still garners relatively high margin (vs. plain vanilla contract manufacturing) as it involves R&D and ownership of IP (intellectual property) of EMS player.

Components EMS players lack capability in making components such as resistors, transistors, diodes etc. Hence, it is mostly sourced from other players globally and domestically. Component manufactures command both high volumes and high margins.

Source: https://www.ourpcb.com/pcb-components.html

Printed circuit board assembly (PCBA) EMS players have been doing large volumes of PCBA in recent years. The market size is estimated at USD25 billion in FY23 and is likely to be ~100 billion by 2030. Hence, this segment has large potential driven by increased use of electronics. Major players - Syrma, Cyient DLM and Kaynes. Margins in this segment are moderate, though sometimes vary based on end-customer industry.

Box build Box build is the final product which comprises of PCB assembly, wiring, welding etc. Indian EMS players are very strong and efficient in box build. Services offered by Dixon and Amber are almost 100% box build. This segment has low margin but high volumes.

Other opportunities PCB (bare board) manufacturing: The overall market for PCB manufacturing is estimated to be USD5billion and India imports over 80% of its PCB requirements. Hence, import substitution and industry growth is likely to result in large opportunities for PCB manufacturers. Amber has built PCB manufacturing capability through an acquisition and Kaynes is also likely to start PCB manufacturing in FY25. Margins in PCB manufacturing is high in 15-20% range vs. PCBA in 5-8% range. Hence, this segment should be keenly watched.

Source: https://www.ourpcb.com/bare-printed-circuit-board.html

Industry

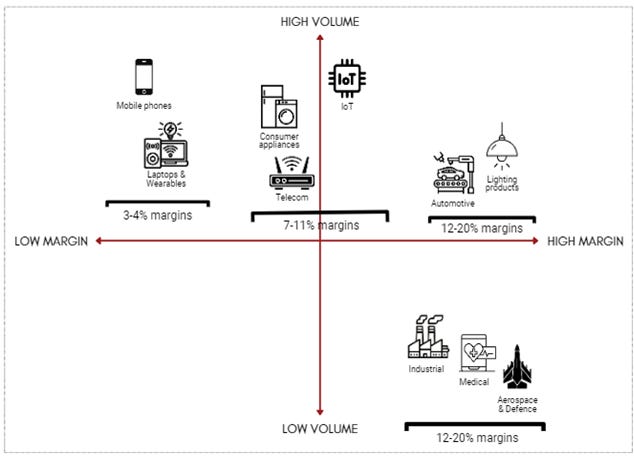

The second factor which impacts EMS growth and margin profile is the end-industry they cater to. Some of end-industries EMS cater to are consumer appliances, electronics (devices/wearables), automotives, healthcare, lighting, IoT, and aerospace & defense. These industries have their own dynamics of volumes and margins. In general, high-volume industries such as mobiles, wearables, laptops etc. are very low margins for EMS companies. Whereas aerospace, defense etc. are low volumes but high margins. It should be noted that criticality and consequences of quality in aerospace and defense industry is high hence margins tend to be high.

Volume and margin mix quadrants

Source: EY, Korman Capital

Level of integration and customization

Other factors such as the level of backward integration, original design manufacturing (ODM), and the degree of customization also impact the margins of an EMS company. For example, IKIO owing to its ODM, customisation and diverse SKUs earns high EBITDA margin of about 20%. IKIO offers smart lighting for home decorative, and aesthetics. The customization caters to specific client needs, adds significant value, and allows companies to charge premium prices. Conversely, Elin, another player in the lighting industry, experiences lower margins due to the absence of some of these factors.

Furthermore, the level of integration aids in improving margins by retaining supplier margins at the EMS level. For example, PG Electroplast has backward integration into plastic moulding, which results in higher EBITDA margins of approximately 10% compared to Amber's 8%.

Study overview

Our study encompassed 10 companies within the EMS sector, manufacturing a diverse set of products and catering to various industries. We have covered Kaynes Technology, Amber Enterprises, Avalon Technologies, Cyient DLM, Dixon Technologies, Elin Electronics, IKIO Lighting, PG Electroplast, Syrma SGS Technology and Inflame Appliances. These companies account for over 90% of market capitalisation of listed EMS players.

Our evaluation criteria included 3 key areas – 1. Earnings (40% weight), 2. Franchise strength (40%) and 3. Valuations (20%). The franchise strength was further bifurcated into gross margins (20% weight), asset turnover (10%), ROCE (10%), ROIC (20%), ROE (10%), cash flow conversion (operating cash flow/EBITDA - 10%) and financial leverage (20%).

There is reasonable focus on OCF for the EMS industry as high growth leads to cash flow issues. In many cases companies have resorted to equity dilution or high leverage (debt) on the balance sheet. These factors in mid to long term can be detrimental for investors.

Story in charts

Earnings

Dixon Technologies is likely to grow at 55% CAGR over the next 3-years, highest among its peers. Average growth across companies is 40%+ owing to industry tailwind and margin improvements.

Source: Korman Capital estimates

*We have excluded Inflame Appliances as it distorts earnings picture owing to its low base/negligible profits in FY24.

Gross margins

IKIO Lighting has highest gross profit margins of 38% followed by Avalon Technologies (34%). IKIO and Avalon both are backward integrated with injection plastic moulding, tooling, PCB design (Avalon), fabrication, assembly, and testing & validation.

In addition, IKIO boasts of 100% ODM manufacturing vs. other companies well below 35%. As a result, IKIO also enjoys highest EBITDA margins (~20%) highest among the companies we studied.

Source: Screener.in and Korman Capital

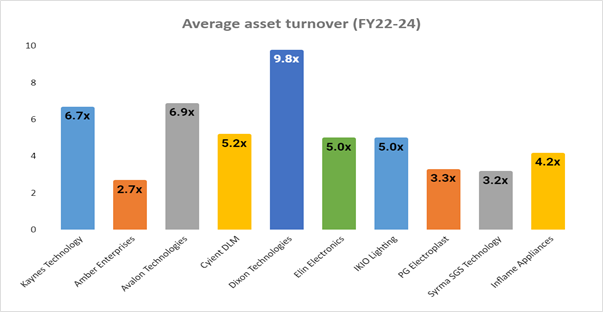

Asset turnover

Dixon Technologies reported the highest asset turnover of ~10x over the past 3-years owing to high volumes and efficient use of assets. Also its worth noting that Dixon’s plant and machinery has high fungibility to switch from one product to other in case demand fluctuates.

Source: Screener.in and Korman Capital

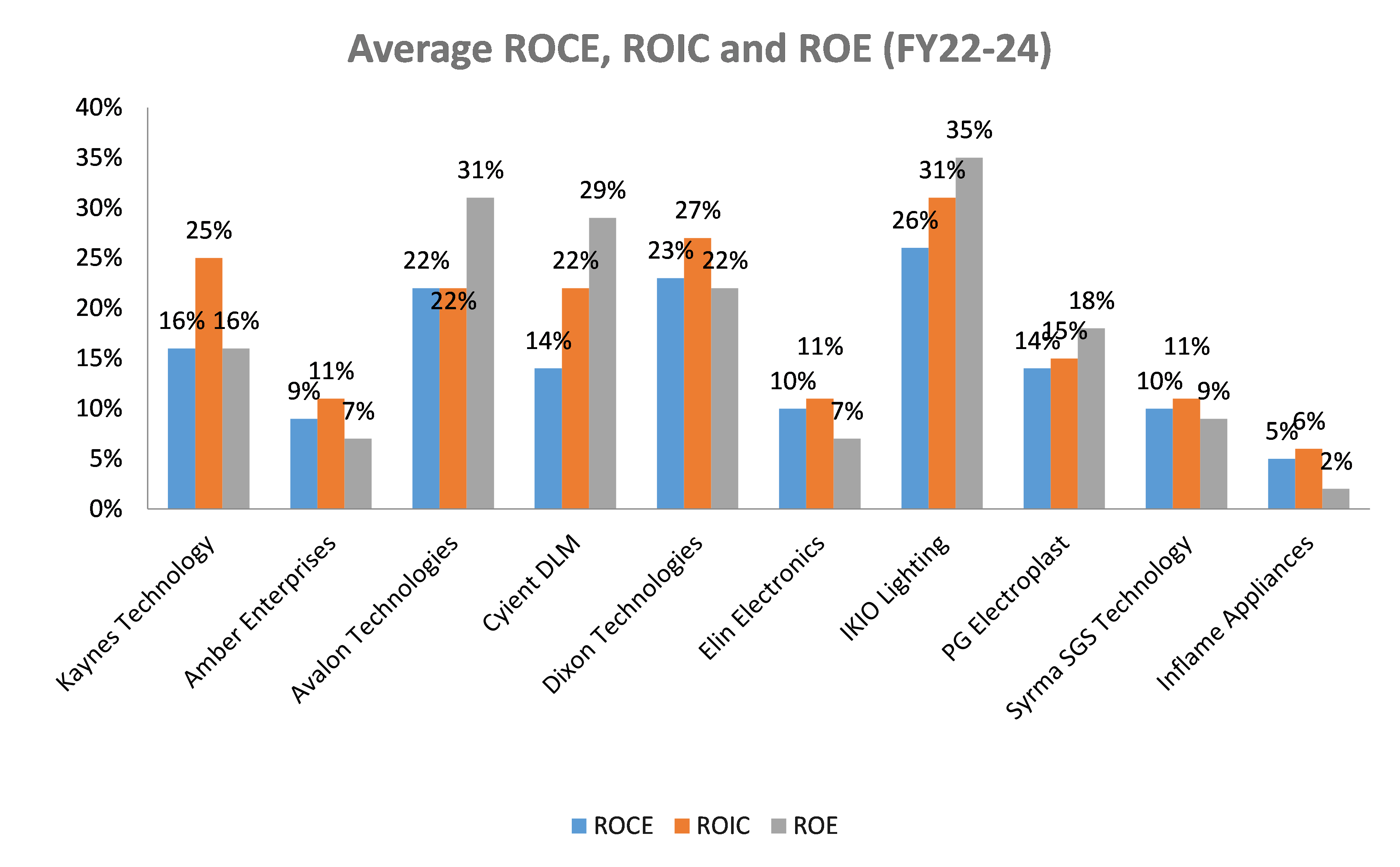

Return metrics

IKIO Lighting is best in terms of returns metrics with ROCE, ROIC, and ROE in 25 to 35% range. This is a largely a factor of its best EBITDA margin. Dixon follow closely with return metrics falling in 20-25% range. Dixon’s returns are mainly driven by very efficient working capital management and cash conversion cycle of less than 10 days vs. peers over 60 days. In addition, Dixon has the best asset turn ratio of ~10x vs. peer average of below 5x.

Source: Screener.in and Korman Capital

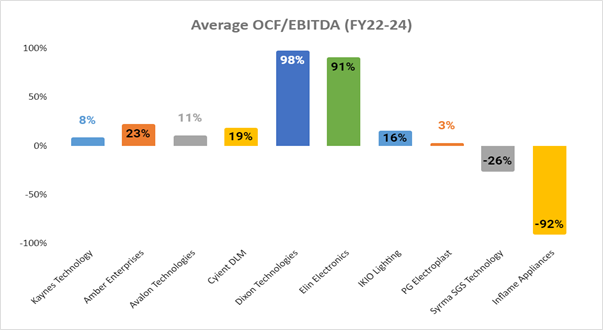

Cash flow conversion

Dixon has the highest OCF to EBITDA ratio (98%) followed by Elin Electronics 91%.

Source: Screener.in and Korman Capital

Valuations

Our focus on valuations is low and account of only 20% of overall weight in the rankings. On the valuation front IKIO leads followed closely by PG Electroplast. Dixon ranked lowest in valuation parameters owing to its high valuations (PE of over 100x, though PEG ratio is ~2x). IKIO and PG Elctroplast are at ~1x PEG ratio.

Outcome of study

Dixon Technologies achieved the top ranking due to its robust franchise and fast growth. Franchise score reflected its high growth and strong return metrics. High valuations did not drag down its rank as valuations weighted lower in our final rank.

Kaynes Technology was ranked 2nd owing to its high growth, good margins, and reasonable return metrics.

IKIO was ranked strongest in franchise strength mainly driven by its high gross & EBITDA margins, high return metrics and negligible debt. IKIO also ranked highest in valuations as its PE ratio stood at 32x vs. peer average over 60x and PEG ratio ~1x.

It should be noted that companies ranking low does not necessarily mean bad companies. The rank is reflective of our preference of growth and franchise strength.

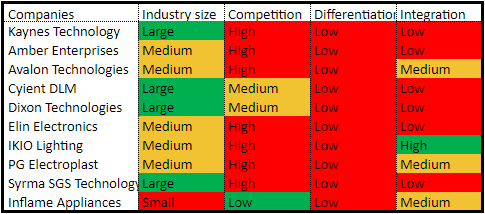

Other factors investors should incorporate are industry size, competition, differentiation and integration to assess the companies. Though all these factors ultimately reflect in margins and return metrics, we believe EMS industry is at nascent stage so current numbers may change the landscape/rankings in 3 to 5 years.

Kaynes, Cyient, Dixon and Syrma cater to large industry however competition and product/service differentiation is low to medium.

Source: Korman Capital estimates/judgement

Conclusion: We believe that Indian EMS industry will continue to grow fast owing to rising demand of electronics, localisation, and government support. Its imperative to select good companies with quality growth (high cash conversion – OCF/EBITDA). As industry is highly competitive and differentiated players will survive for longer. We believe Dixon has created a highly efficient business in mobile manufacturing however valuations remain a question mark. Cyient DLM is largely getting its revenues from aerospace and defense which are critical components.